Retirement provision for freelancers has been a hot topic in recent months. The number of Germans becoming self-employed is increasing. Compared with employees, freelancers in particular need to examine many ways of securing their retirement and begin making provisions early.

Especially because of the continuing low-interest-rate phase and the falling pension level, alternative asset classes are of great importance for long-term and secure retirement planning.

We will cover the following topics:

Transparency note: The information mentioned has been summarized to the best of our knowledge and belief; no liability is assumed. As the legal situation is constantly changing, ElevateX GmbH as author does not provide investment advice. Status: 24.02.2021.

Statutory pension insurance - mandatory or not?

In principle, freelancers usually have a wide range of options when choosing how to invest in retirement provision. In Germany, statutory pension insurance is the central old-age security system for employed people and is administered nationwide by Deutsche Rentenversicherung Bund, based in Berlin.

Although statutory pension insurance is mandatory for every employee, freelancers are usually only mandatorily insured in the statutory pension scheme under certain conditions. As a result, freelancers are themselves responsible for making provision for old age. Even though statutory pension insurance is not generally a must for the self-employed, some freelancers are obliged to pay into it. Insurance obligations apply, for example, to education and care professions.

This blog article is primarily concerned with how freelancers who are not subject to compulsory insurance, for example freelancers in IT, can structure their retirement provision.

Duty: make provision appropriately, in good time, and in a targeted manner!

As a basic rule, all freelancers are responsible for taking care of their retirement provision in an appropriate, timely, and targeted manner. A wide range of retirement provision options is available, and in some cases they can be combined. According to surveys, German freelancers especially favor statutory and private pension insurance, life insurance, securities, and real estate.

Statutory pension insurance (GRV)

A central branch of the German social security system is statutory pension insurance, which serves in particular to provide retirement income for employees. Statutory pension insurance works on a pay-as-you-go system: pension contributions paid by people currently in work are paid directly as pensions to current pensioners. This is known as the intergenerational contract, meaning that the generation of those in work supports the generation of those retired at the same time - a very social and at least theoretically permanently functioning principle.

Demographic change and the overburdening of future generations pose major problems for the pension system, especially in Germany. According to experts, in 20 years at the latest one employee will have to finance two pensioners - as a result, the mathematical formula of pay-as-you-go financing can no longer hold and the pension level is falling increasingly.

The contribution rate to pension insurance remains stable at 18.6% in 2021, resulting in monthly contributions of at least EUR 83.70 and a maximum of EUR 1,283.40. Freelancers choose the amount of these contributions themselves in the case of voluntary pension insurance, and they can also decide how often the contributions are paid.

Advantages

- Guaranteed monthly pension payments

- Ability to claim tax advantages

- Support measures in case of health-related work restrictions or absence

- Orphan’s and survivors’ pensions for relatives in the event of death

- Possibility of linking payments from a classic employee relationship

Disadvantages

- Falling pension level

- Comparatively low return

- Subject to income tax

- Long-term risks in financing the pay-as-you-go system

Ultimately, the state pension is usually not enough as the sole pillar of retirement provision. For this reason, the state explicitly recommends additional provision and building a second pillar alongside statutory old-age provision.

Private pension insurance

An alternative to statutory pension insurance is private pension insurance. The difference compared with the statutory scheme lies in the fact that the pension is calculated using the “pension formula”, whereas the amount of private pension insurance depends on the respective contract design. Paid-in savings contributions are credited with a guaranteed interest rate, reduced by sales and administration costs charged by the provider. Surpluses are often paid out to policyholders, which increases pension payments. However, the contract holder is only guaranteed the “guaranteed pension” specified in the contract. In this sense, private pension behaves like a savings contract in which the provider invests the payments profitably.

The state promotes various forms of private pension insurance for retirement provision. These include the Rürup pension or basic pension, as well as the Riester pension and Wohnriester. In addition to classic private pension insurance and occupational pension provision, variants based on unit-linked pension insurance are also available. Policyholders can choose between two variants - a deferred and an immediately starting pension policy.

Important: Contributions during the savings phase can be claimed in the tax return as special expenses up to EUR 1,200. The tax amount for pension payments received in retirement depends on the age at which the pension starts - the older you are when you retire, the lower the tax burden. For private pension payments, only the taxable portion of the return is taxed. This is higher the younger the pension recipient is when the pension begins. Private pensions, like statutory pensions, are guaranteed for life. They can be supplemented with additional insurance for disability, accident, or long-term care.

Life insurance

Life insurance, like all investment instruments suitable for retirement, is another form of long-term money investment. Here too, money is paid in over a period of years, invested at a fixed interest rate, and paid out when retirement age is reached. The difference compared with pension insurance is that the accumulated money can be paid out in one lump sum. Life insurance also includes death benefit protection. In that case, the insured person’s family receives the insured amount if the insured person dies before retirement age.

Note: both pension insurance and life insurance have long been criticized for a lack of transparency in profit distribution and are becoming less attractive due to low interest rates.

Securities: shares, ETFs, funds

Surveys on freelancers’ retirement provision show that securities are also highly popular. This is especially due to the high return potential that money invested over a long period can achieve through securities. Although the securities market is subject to larger short-term fluctuations, money invested over a long period yields the greatest profit. A long investment horizon therefore smooths out temporary highs and lows.

In principle, you no longer need deep knowledge of companies or the stock market in order to invest, because numerous expert-managed investment vehicles handle this work. However, super-investor Warren Buffett famously said: “Never invest in a business model you don’t understand!”

Today’s market offers a wide range of funds and other investment opportunities to benefit from the growth of global stock markets and build solid retirement provision. In recent months in particular, interest in investing in shares has also risen sharply in Germany, because returns in recent decades have been higher than in almost any other investment option.

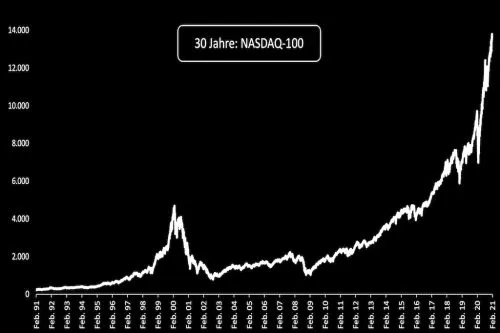

An investment in the world’s largest technology index, the NASDAQ-100, would have produced a return of more than 5,400% over an investment period of 30 years, meaning that an investment of EUR 50,000 would have become EUR 2.7 million.

Especially with securities, it is very important that investors start early and continue investing regularly, for example in funds, because over the longer term this makes the eighth wonder of the world, the compound interest effect, even more effective, alongside the benefit of balanced payments and avoiding market fluctuations. Historically, return-oriented asset classes such as shares and equity funds have achieved significantly higher returns than inflation over the long term - so the purchasing power of the assets is preserved. As retirement approaches, there is enough time to shift into lower-volatility and therefore even safer investments and reduce risk.

Depending on how risk-tolerant you are as an investor and what return expectations you have, different investment options become available. The most popular asset classes are shares, ETFs, and funds. A securities portfolio is often also supplemented with commodities, real estate, and cryptocurrencies.

Investments in shares are, according to the returns of recent decades, the most successful asset class. In principle, there are three options here. You can invest in individual stocks. This means that you have to analyze companies yourself and buy shares. Naturally, volatility is higher with only a small number of shares than with the second option, ETFs.

An ETF (“exchange traded fund”) is a stock market-traded index fund that tracks the performance of an index such as the DAX or the NASDAQ 100. In this case, you invest in a fund that mirrors the price performance of the 30 companies in the DAX as closely as possible, for example. This means you are diversified across 30 companies at the same time.

A third way to invest in shares is through classic actively managed funds. In this case, a fund manager decides which individual stocks become part of the portfolio and in what proportions. As a result, investors typically pay a percentage-wise higher management fee than with ETFs - although, after costs, very few funds consistently outperform ETFs.

It is also useful to know that for some time now it has been possible to set up savings plans. These allow you to invest a fixed amount automatically every month on a specific date in individual shares, ETFs, or other funds.

Commodities

Commodity investments have a reputation as a speculative instrument with high risk. Commodity prices are volatile because they depend on many different factors that private investors often find difficult to assess. Nevertheless, when used carefully, they can contribute to the overall stability of a securities portfolio. Commodity prices often move in the opposite direction to the rest of the market. Gold is not called a “safe haven” in times of crisis for nothing. That is because a precious metal does not generate interest. The lower the interest rate level, the more attractive a gold investment becomes.

Whether gold, silver, or oil, it is of course also possible to invest directly in companies - i.e. shares - that work in the gold or oil business, for example. This is particularly beneficial for risk-averse people.

Cryptocurrencies

Cryptocurrencies - or simply “cryptos” - are everywhere in the media. Is it advisable to invest in virtual money, and are digital currencies a new financial instrument?

In fact, the purposes of crypto technology differ: some are stores of value, others are means of payment, and still others are intended to help accelerate the energy transition. At present, hardly any investment is riskier than cryptocurrencies. Nevertheless, investors agree that cryptocurrencies will play a major role in the future - the only question is whether they will remain as decentralized as they are today and what their purpose will be. As a speculative investment with considerable upside potential, you can allocate a small part of your portfolio to crypto, but as always, the loss should be bearable.

The same applies here: only invest in the asset classes you understand yourself. Whether Bitcoin, Ethereum, or Cardano, you should understand the investment you are making and the company or technology behind it.

Real estate

Finally, real estate is still regarded by freelancers as a safe investment and a form of retirement provision. Surveys repeatedly show that real estate is even the most used form of retirement provision. Important factors when buying property include whether owner-occupation or letting is the focus, and aspects such as infrastructure, quality of life, and local jobs. The basic rule for searching for property is: take enough time. Ideally, you should observe the property market for a few months. This will gradually give you a feel for property prices in the region you have selected.

Conclusion

Every freelancer should think about retirement provision early on. Often, voluntary payments into the statutory scheme are not enough to ensure a good standard of living in old age. A well-thought-out strategy based on several pillars is therefore sensible for all freelancers and beyond. All investment forms are associated with risks as well as advantages and disadvantages, which is why diversification and building multiple sources of income are essential for retirement provision.

Would you like to know more about retirement provision or other questions relating to freelancing? Do you have suggestions, praise, or criticism about the article? Then feel free to get in touch and book an initial consultation call with us!

![Agentic Engineering Hiring Interview 2026 [+21-Question PDF]](/_astro/agentic-engineering-interview-featured-de.BlvVAp5j_Z9ib7o.webp)